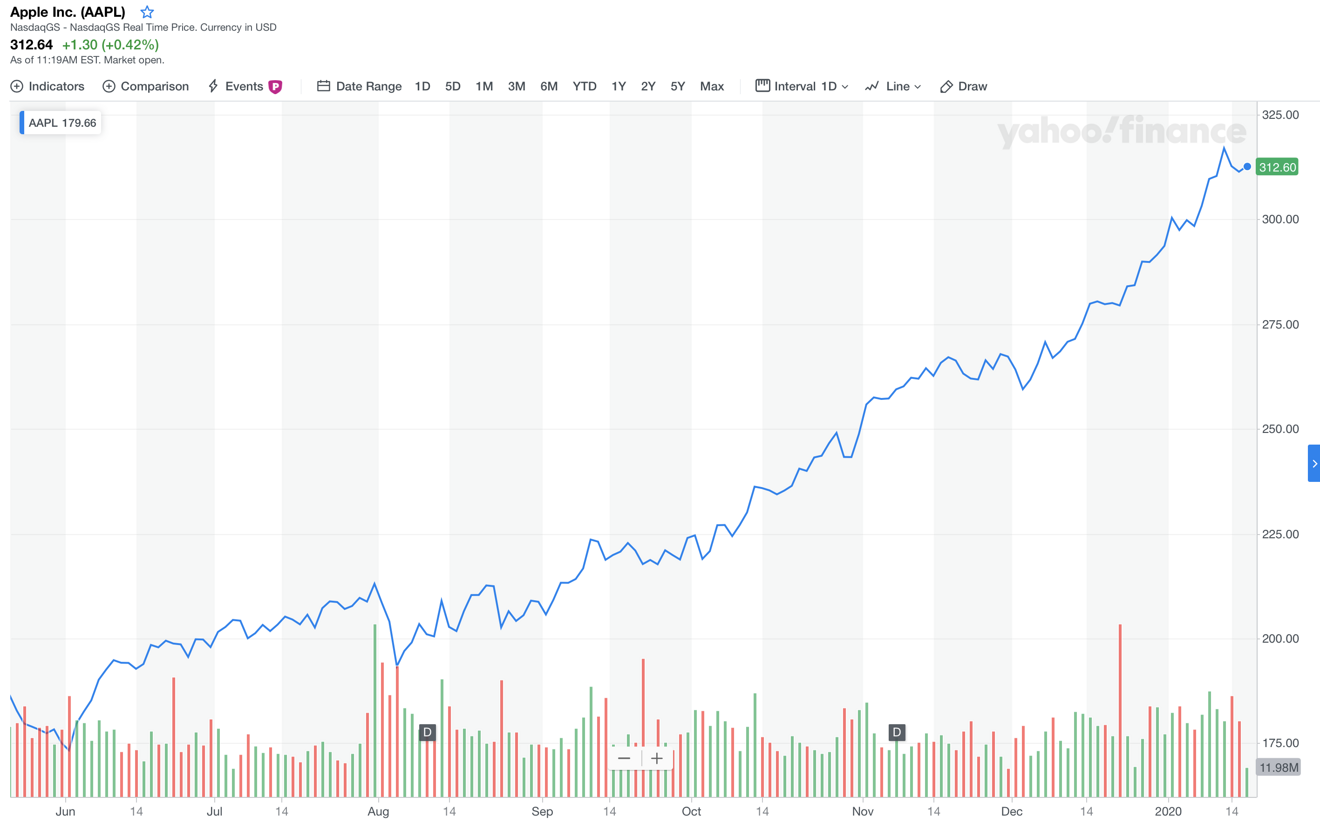

Investors are waking up to Apple's new valuation

Apple's shares have more than doubled over the last year, but the rapid increase isn't just the result of some temporary irrational exuberance. Instead, as a variety of analysts and observers have noted, it means that investors have formed a new understanding of Apple as a company, shedding their formerly bleak pessimism that valued Apple far lower than the various consumer electronics rivals it has been outperforming.

Why Apple's stock valuation matters

Understanding what is happening to Apple's share price should be of interest to more than just the investment community. For Apple's customers, it's an endorsement of the company's long term strategies that have produced a string of hit products. It indicates that Apple wasn't merely one-time-lucky creating its iPhone and iPad at just the right times, and is instead capable of plotting out a sustainable, strategic array of products and services that can be both profitable and well-received.

Apple is operating globally as a precision engine that's adept at delivering the future. The same can't be said of Microsoft, Google, Samsung, and other Android licensees. They have all jumped back and forth between strategies and various trial initiatives without following through, often ultimately abandoning their ideas after failing to finish them or simply being unable to find a large enough audience to sustain them.

From Surface to Windows Phone, and from Nexus and Pixel phones, tablets and netbooks to Galaxy Edge, curved screens, 3D, gesture detection, insecure biometrics and so on, the rest of the industry sits in stark contrast to Apple's decades of consistent blockbuster hits and solid technological milestones.

Apple has made mistakes, canceled plans, and backtracked in its direction, but those events stand out as aberrations. Virtually every significant thing the company has delivered over the past two decades has ramped up into a multi-billion dollar enterprise. Android, collectively, has largely been a failure outside of phones. And all the phone makers in China put together are earning less money than any of the various fledgling initiatives Apple has launched recently. That's incredible.

Apple's successes include year after year of innovative iPhone models that continue to set—and raise—the bar in how smartphones are designed and what features are important on a global scale. They also involve new types of wearables from Apple Watch to AirPods, as well as unique features from Sidecar and Continuity Sketch to AirPlay 2 to its wearables' secure health monitoring, EKG, and fall detection—features that are not just novel but are saving lives.

Android Wear, Microsoft Band, and Samsung Gear all failed to have had any real positive impact on users, in addition to being commercial failures for those companies.

These facts matter, and finally, for the first time in a decade, Apple's valuation as a company is beginning to reflect this rather obvious reality. Why has it taken so long?

Why Apple's stock has been undervalued for so long

It certainly appears that Apple's historically low valuation in terms of Price to Earnings—its stock valuation compared to its ability to generate profits—is tied directly to one of the largest mistakes made by tech industry investment analysts over the past decade: the idea that Apple's iPhone was a fluke product that would rapidly be commodified and overrun by an army of cheaper, less restricted and more "open" handsets running Google's Android.

This assumption was grounded on the 1990's history of the Macintosh, which began to perform well for Apple for just a few years before Microsoft copied its foundational concepts and spread them across generic PCs, erasing much of the value Apple had created. For many users, Windows PCs served their needs better than a Macintosh could, resulting in Apple being relegated into a niche role in certain creative and education markets.

Virtually every analyst following Apple used that history to predict that the same thing would happen to the iPhone at the hands of Android. However, something else began happening that should have affected their outlook a lot earlier. In the 2000s, even before iPhone shipped, Steve Jobs' Apple began turning the Macintosh around from being a niche PC into being a desirable premium product that stood out among generic Windows PCs. Even more importantly, the company also began selling massive quantities of new iPod devices, which various rivals tried to copy without achieving similar success.

In 2007, the iPhone combined the desirable ease of use of the Mac with the attractive industrial design and simplicity of the iPod to deliver the first modern smartphone to sell to mainstream users. But rather than observing these events and envisioning the global superpower that Apple subsequently developed into after the initial launch of the iPhone, something very different occurred.

Why most analysts got Apple wrong

As recently noted by Asymco analyst Horace Dediu and Beyond Avalon analyst Niel Cybart, in 2008 Apple's P/E had historically hovered around 40. But within 2008, Apple's stock price crashed in half twice, as other analysts began anticipating that Apple's new hit product was about to be blindsided by the erupting Great Recession. Who would buy a premium-priced phone as "global macroeconomic conditions" worsened?

It turned out that iPhone was far more valuable than the supposedly premium price Apple was asking—a price that most carriers were subsidizing anyway. iPhone sales took off and never looked back, growing at astounding rates for the next ten years. Across that entire period, however, media bloggers kept pushing a narrative that someday soon, Apple would run into overwhelming competition that it would be ill-equipped to handle.

It was first imagined that Palm could, with the help of a large number of defecting Apple employees, deliver a better smartphone. It was then thought that Blackberry could leverage its tight relationships with the enterprise to stop Apple's rise. Then Microsoft was seen as capable of spending billions of dollars to deliver a better phone experience, somehow leveraging its Windows platform.

Eventually, as every other credible competitor faded, it was assumed that Google could unite all the failed phone makers into one glorious free and open platform following the model of Windows in the 1990s. That illusion lasted the longest, with proponents even today suggesting that an odd feature here or there was finally going to "take on" Apple's iPhone. It never happened despite ten years of credulity-level optimism entertaining the idea.

What did happen was that Apple began taking the offensive, pushing into areas where other phone makers had established some niche. It first hit Samsung's big-screen phablets, then the enhanced camera features offered by Nokia and Sony, moved on to create an ecosystem of business apps once owned by Microsoft, and most recently pushed into wearables introduced by Fitbit and others.

Apple proved that it could not only survive, but that it could inhale entire business segments, leaving no room for competitors.

As the decade progressed, the idea that some western competitor of Apple was going to slow its roll was given up on, and the focus moved first to Samsung, then to various companies in China: Xiaomi, Oppo, Lenovo and most recently Huawei. Looking only at shipping unit volume, it's possible to contrive a story where Apple is indeed falling behind in smartphone market share.

However, global unit sales didn't have any negative impact on iPods in the previous decade of the 2000s. Tons of cheap MP3 players didn't slow Apple's growth in the slightest. What was more important to Apple's success back then with iTunes and iPod was its loyal user base, not the relative percentage of all the world's MP3 players that were being shipped by Apple.

In 2014, Apple's chief executive Tim Cook began directing increased attention to this reality, noting that unit sales alone were not providing an accurate assessment of Apple's current or future business prospects. Huge numbers of low-end handsets being shipped into India and remote areas of China and other emerging markets were not stopping Apple's ability to sell its premium quality iPhones to the most commercially significant buyers in urban areas, no matter how many market research groups could crank out misleading statistics that indicated that some other company was "leading" smartphones by shipping out millions of low quality, commodity devices that were not earning money nor even creating a favorable impression among their users.

The ignorant and often cynical pessimism of tech media kept insisting that unit shipments and overall market share were critically important, and that they showed beyond a doubt that millions of users somewhere were leaving Apple's ecosystem to buy cheaper Huawei devices. Beyond minor bloggers, this story was paraded around by the New York Times, by Bloomberg, Japan's Nikkei, and by other major news outlets.

Analysts too parroted off truths-sounding reports that claimed that nobody could possibly be buying Apple's $999 iPhone X and that logically it just made sense that everyone was buying Huawei's instead. Except that wasn't happening. Some even made up data that supported this narrative.

Just a few weeks ago, Rosenblatt Securities analyst Jun Zhang issued a report that claimed that sales of the new iPhone 11 were troubled, causing Apple to slash production orders by 30 percent, all based on the same "channel checks" that have been proven to be utterly wrong data year after year after year.

Barely one month ago, the New York Post produced an article that claimed, base on the Rosenblatt report, that "Apple sees iPhone sales continue to slide in China," warning that "Demand for the latest iPhones is plummeting in China, leading Apple to cut back production."

A variety of other news sources cited Rosenblatt's conjecture as fact. Still, just weeks later, the Chinese government released data showing that those channel checks had no basis in reality whatsoever. Rather than being a colossal failure, iPhone 11 sales in China had grown by 18 percent over the previous year.

More importantly than the number of units Apple is selling is the increasingly evident reality that Apple is building a solid ecosystem around iPhones, selling its buyers other products, apps, and subscription services that Android is not capable of replicating. Now that investors are seeing further proof that Apple is functionally servicing a massive installed base of users, rather than just selling another wave of phone units, the P/E valuation they are assigning to the company is resulting in a massive increase in the share price.

Apple's current P/E of around 26 is double where it has been across much of the last decade, but is still undervalued when compared to Google (28) or Microsoft (31). That indicates that the company's massive jump isn't out of the ordinary, but rather a long-overdue correction. It also indicates that Apple's executives were right when they claimed that the company was undervalued and that the best use of the company's cash was to buy back shares and retire them, transferring that value to their shareholders.

To anyone who listened, that clearly articulated message has proven to be a huge windfall, creating massive billions of capital for shareholders who stuck with the company.